mutual funds sahi hai...!

mutual fund

Mutual funds are the most neglected instruments , it’s crucial to understand the advantages they offer before diving indepth .

- Funds are managed by professional managers.

- Higher returns historically, better than gold, FD, RD, real estate.

- Availability of different funds as per risk appetite.

- Easy to invest , availability of SIP & SWP.

- Minimum investment can be as low as 500.

- Beats inflation.

- Benifit of Tax saving.

- provides high liquidity.

- Schemes for Every Financial Goals.

- No need to track the stock market.

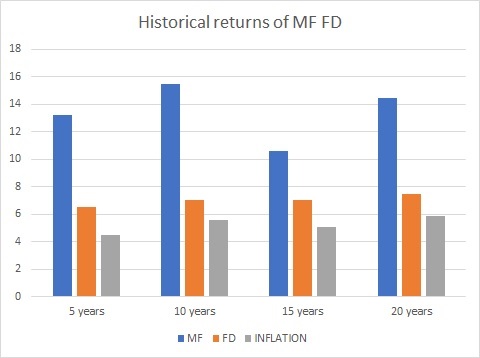

Historical returns of Mutual Funds vs Fixed Deposits .

The below chart shows the % return of FD & mutual funds in addition to inflation. Mutual funds (MF) have given higher returns consistently over the last 20 years. Even then significant % of money is still in FD this is because of a lack of awareness. One should start investing in MF for better returns with quantifiable risk.

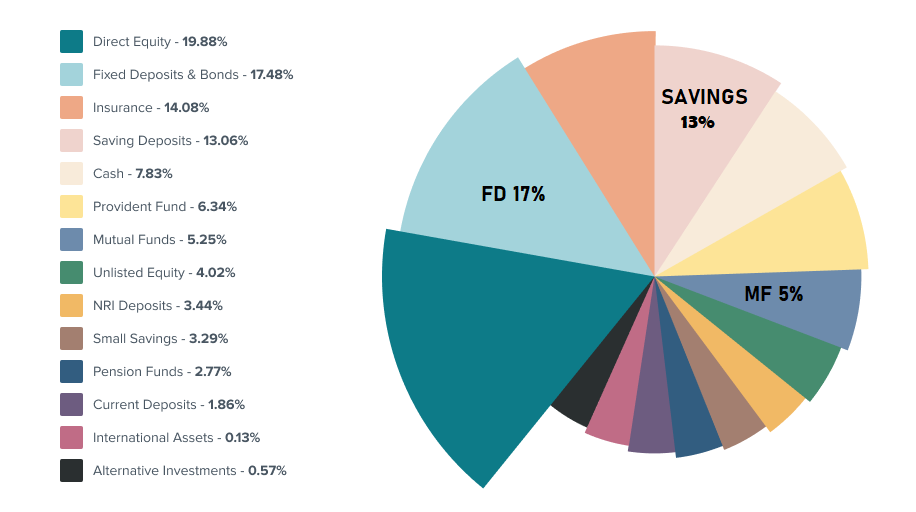

Investing pattern of an individual .

The below chart shows how an individual is investing in the different instruments even though mutual funds (MF) give higher returns, savings and fixed deposit still accounts for 30% whereas mutual funds are a meagre 5%. this is because of a lack of awareness. a significant percentage of money can be moved from savings & FD to MF for better returns.

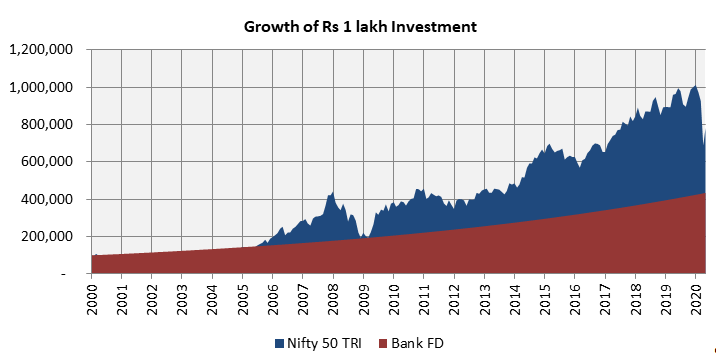

Comparison 1 lakh invested in Mutual fund vs Fixed deposit.

If Rs 1 lakh is invested for ten years, an FD will pay you Rs 1.79 lakh (assuming 6 per cent returns). However, if you invest the same amount in large-cap mutual funds, it will become Rs 3.75 lakh (assuming 14 per cent returns, which is the average of all large-cap mutual funds return in 10 years). This is almost 190 per cent of FD returns.

The below chart shows how mutual funds (MFs) performed across different categories over the past 10 years. The list shows the performance of a few funds in the category, however, the average shows not only listed funds but across the mutual fund category average. By looking at the below chart one should understand, in the long run mutual funds are the best investment instruments. so every time one thinks of investment one should look at the opportunities offered by mutual funds.

Historical 10 years performance of Mutual funds May 2025.

Comparison SIP ( Systematic Investment Plan ) in Mutual fund and Fixed Deposit.

The below example shows how much difference it makes in the long term. When 10000 invested in SIP ( Systematic Investment Plan ) over 25 years in mutual funds and in FD ( fixed deposit ), MFs give 3 times more return than FD. which is 1,57,49,781 ( 1 crore 57 lakh 49 thousand ) more than FD, which is phenomenal.

Key Observations:

PPF & SSY offer stable but lower returns (~7-8%), with tax benefits (EEE status).

NPS (Equity-heavy) has given higher returns (~10-12%) but comes with market risks and tax complexities.

Fixed Deposits provide safe but low returns (~6-7%), taxable as per slab.

Equity Mutual Funds have outperformed with ~12-18% returns over long periods but are volatile.

Debt Mutual Funds offer moderate returns (~6-8%), better than FDs post-tax for higher brackets.

Gold (SGBs) has given ~8-10% returns, acting as a hedge against inflation

Why Mutual Funds Are the Best Investment Instruments in India

Mutual funds have emerged as one of the most efficient and rewarding investment avenues in India. Whether you’re a beginner or a seasoned investor, they offer a perfect blend of diversification, professional management, and long-term wealth creation.

Superior Returns

Historically, equity mutual funds—especially large-cap and small-cap—have delivered significantly higher returns compared to traditional instruments like FDs, PPF, and even NPS. Over long-term horizons (5–10 years), they have consistently beaten inflation and created substantial wealth.

Low Entry Barrier

You can start investing with as little as ₹500/month via SIPs (Systematic Investment Plans). This makes them accessible to everyone, regardless of income level.

Diversification & Risk Management

Mutual funds spread your money across various companies, sectors, or debt instruments, reducing risk. This diversification is hard to achieve when investing directly in stocks or bonds.

Tax Efficiency

Equity mutual funds held for over one year qualify for long-term capital gains tax, which is only 10% above ₹1 lakh gains—much more efficient than the tax on FDs or rental income.

Professional Fund Management

Your money is managed by expert fund managers who use research, analysis, and market insights to make smart investment decisions—so you don’t have to.

Regulated and Transparent

All mutual funds in India are regulated by SEBI, ensuring investor protection, transparency in performance reporting, and regular disclosures.

Pension planning & goal-based investments

One needs to accumulate part of savings over a long period so that one can have a secured financial future. It helps you to deal with the uncertainties of post-retirement and ensures a steady flow of income. Savings get exhausted very fast and are sometimes used in emergencies, Money should help you achieve your life goals, having plans at the early stage and working towards them will help you to avoid the burden in the future.

Some of the major events that have to be planned are listed below, either retirement or below listed events Mutual funds can be effectively used to achieve the goals.

- Retirement planning

- Children’s marriage

- Children’s education

- Starting a business

- Buying a house

- Aiming for early retirement

- International holiday

To conclude Mutual fund is a powerful investment option that has the potential to generate long-term wealth for investors. It offers many advantages and benefits whether it is liquidity, diversification, ease of investment, flexibility to invest in smaller amounts, schemes for every financial goal more importantly safety and transparency.